Let’s start by reviewing some of the most common terms, such as co-pay,

Did you know?

Open enrollment is November 1 – January 15. Compass is here to help you understand your insurance options.

Depending on your particular situation, you may have options when it comes to choosing your health insurance. Your employment status, household size, and income, all play a role in your options. The four primary types of insurance are employer-based plans, plans on the

Employer-Based (Group) Plans

In the United States, most people have health insurance coverage through their own or a family member's employer. Employer-based health insurance, also called a group plan, is selected and purchased by an employer and offered to eligible employees and their dependents. Any businesses with 50 or more full-time employees is required to provide health insurance to their employees. Your employer will typically share the cost of your

There are two types of employer-based coverage:

Fully funded group plans : The employer purchases coverage from an insurance company and the insurance company processes and pays health care provider claims.- Self-funded group plans: The employer sometimes assumes the role of the insurance company, and processes and pays health care provider claims. However, in some cases, there may be a third-party administrator that assists with health insurance claims. For self-funded plans, it is often up to the employer to decide whether to cover a service. In most cases, appeals are made directly to the employer's human resources (HR) department.

COBRA

The Consolidated Omnibus Budget Reconciliation Act (COBRA) is a form of employer-based coverage that gives employees and their families the option to extend their insurance if they lose job-based health coverage, such as by leaving their job or getting laid off. An employer is required to offer COBRA if it has 20 or more employees on more than 50 percent of its typical business days. Most qualified individuals are required to pay the full cost (which cannot exceed 102 percent of the premium, or the full cost of the coverage plus a two percent administration charge) of the plan. Because employers typically cover part of the premium while the employee is working, the cost of continuing coverage through COBRA can be significantly greater. COBRA coverage can continue for up to 18 months. Once you opt into COBRA, you cannot drop it and switch to a Marketplace plan until the following year or until the open enrollment period. This is because a voluntary loss of coverage is not considered to be a qualifying life event for the

Those who do not choose to take COBRA coverage can

Health Insurance Marketplace Plans

The Health Insurance Marketplace, also known as the Health Insurance Exchange, provides people a way to buy a plan if they do not have access to group-based employer plans or do not qualify for Medicare or Medicaid. To access your state's Marketplace, visit healthcare.gov.

Typically, Marketplace insurance plans are grouped by levels of coverage named after different types of metals:

- Bronze plans offer the least coverage but also have the least expensive monthly premiums. On average, you will pay 40 percent of your health care costs with a bronze plan.

- Silver plans will usually require you to pay 30 percent of your health care costs.

- Gold plans typically require you to pay 20 percent of your health care costs.

- Platinum plans offer the most coverage but also have the most expensive monthly premiums. On average, you will pay 10 percent of your health care costs with platinum plans.

You can only buy a new plan or make changes to an existing Marketplace plan during the annual open enrollment period period unless you have a life event that qualifies you for a special enrollment period.

Marketplace Subsidies

Based on your household size or income, you may be eligible for cost savings in the form of a tax credit to lower your monthly premiums. You can qualify for a premium tax credit if your household income range is between 100 percent and 400 percent of the Federal Poverty Level (FPL). For more information on eligibility, visit the Saving Money on Health Insurance section on healthcare.gov.

Marketplace plans also offer access to cost-sharing reduction plans. These are specially designed Silver-level plans with lower co-pays and deductibles. These plans are only available to people with incomes between 100 percent and 250 percent of the FPL. Individuals who fall within this category can take advantage of the premium subsidy at the same time, significantly lowering cost for health coverage.

Private Insurance Plan

Private or off-exchange insurance is provided by nongovernmental sources, such as private insurance companies. Individuals can purchase these plans through a broker or directly from an insurance company outside the marketplace. These plans vary greatly in what services are covered, premiums, and other

Public Insurance Programs

Public health insurance programs are government-funded and provide health care assistance to qualifying individuals and their families. These programs include:

- Medicare

- Medicaid

- U.S. Department of Veterans Affairs

- Children's Health Insurance Program (CHIP)

- Department of Defense TRICARE and TRICARE for Life programs

- Indian Health Service (IHS)

Many states also have CF-specific programs such as programs for children with special health care needs (sometimes called CSHCN programs). In most states, families that do not qualify for

Primary Versus Secondary Insurance

Many people with cystic fibrosis report having more than one form of health insurance coverage. In these cases, you will have both a primary and a secondary insurance provider and your benefits must be coordinated to ensure you receive maximum coverage.

Your primary health insurance plan is the first to pay for services or treatments you receive. If the primary plan does not cover a service or treatment completely or at all, then your secondary health plan or program may cover it. It is important to notify both plans, so that coordination of benefits can be set up correctly. If the

Learning more about the structure of plan types can help you make the most of your coverage and evaluate your options.

A provider network is a set of doctors, hospitals, clinics, and other health care providers that are contracted with your health insurance plan to provide care at a reduced cost. Most health plans use a network. Because CF care teams are important for people with CF, knowing whether your CF care center is included in a plan's

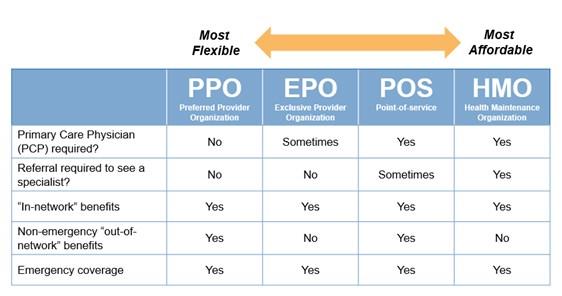

Health Maintenance Organization

A health maintenance organization (HMO) plan limits coverage to health care providers who are contracted with the HMO network. The plan covers care only from providers in the network and does not pay for care from the providers outside of the HMO network, except in an emergency. HMOs require you to choose a primary care physician (PCP) who must then give you a referral to see any specialist. Without a referral, HMO plans do not cover care from a specialist and you will be responsible for most, if not all, of the associated costs.

The primary benefit of HMOs is that they have lower premiums and may have low or no

Although HMO plans may feature lower health insurance costs up front, they can be more restrictive in covered services and how they are accessed. When you are considering an HMO, it’s important to make sure your CF care is covered.

Preferred Provider Organization

A preferred provider organization (PPO) plan provides coverage for the services obtained from providers outside of a plan's network. With PPO plans, you pay less for care from in-network providers but can still receive coverage for out-of-network care without a referral at an additional cost.

PPO plans generally provide more flexibility than HMO plans. However, they often cost more. If you

Exclusive Provider Organization

Exclusive provider organization (EPO) plans combine the flexibility of a PPO plan with the cost-saving benefits of an HMO plan by giving you the freedom to choose any provider within an EPO network without selecting a PCP. In addition, EPO plans do not require referrals from a PCP to see a specialist.

It is important to note that EPOs do not cover the services obtained from providers outside of the plan’s network. When selecting this plan, it is important for you to confirm that your CF providers are in-network before enrolling. If you do go to a doctor or hospital that does not accept your plan, you will be responsible for paying all care-associated costs.

Point of Service Plan

A point-of-service (POS) plan combines different elements of HMO and PPO plans. Like an HMO plan, you must choose a PCP, but you can also go outside of the provider network for health care services with greater out-of-pocket costs, like a PPO plan. Services provided by the PCP are typically not subject to a deductible, and a wide range of preventive care benefits are also included.

The primary benefit of a POS plan is that it offers a “middle of the road” option in which you have more choices than what an HMO plan typically offers while you pay less than with a PPO plan.

High-Deductible Health Plans

A health savings account (HSA) is a tax-exempt medical savings account that is paired with a high-deductible health plan. It’s a personal bank account to help you save and pay for covered health care services and qualified medical expenses. You must sign up for a high-deductible health plan that meets a deductible amount set by the Internal Revenue Service (IRS). The IRS sets a limit on how much you can put into it each year. For more information, visit the Health Savings Accounts section on irs.gov.

You may also be eligible for a flexible spending account (FSA) or a health

Almost every insurance plan has a set of defined pharmacy and medical benefits. Understanding how your plan's pharmacy and medical benefits will be handled by your health insurance provider is an important aspect of choosing the right plan.

Understanding Medical Benefits

A plan's medical benefits are primarily for services such as care center visits, hospitalizations, in-home intravenous (IV) services, medical devices, therapies, respiratory therapies, procedures, and lab work. Any service that falls under the medical side of your plan's benefits is subject to the medical

Understanding Pharmacy Benefits

A plan's pharmacy benefits determine the level of coverage for prescription medications. Most health insurance plans have a tiered structure for pharmacy benefits, offering different co-pay amounts that increase in price as you move through each tier. Most plans have three to five tiers for prescription medications. For example:

- Tier 1: Generic medications (least expensive)

- Tier 2: Preferred brand-name medications

- Tier 3: Non-preferred brand-name medications

- Tier 4: Specialty medications (most expensive)

Because each tier has different associated costs, it is important to know which tier your medication is in before selecting a plan. Even though a plan's Summary of Benefits may list a certain co-pay amount for prescription medications, this rate will likely not apply if your medication falls under a higher tier.

Specialty Pharmacies

A

- High-cost drugs

- Services such as refill reminders, overnight deliveries, and online prescription tracking

- Therapy management to ensure

safety and compliance

Medications from specialty pharmacies typically need to be handled and stored in a particular way to maintain effectiveness. Your insurance plan may require you to use a certain specialty pharmacy.

Insurance is complicated. To learn more about your insurance options and coverage:

- Contact CF Foundation Compass at 844-COMPASS (844-266-7277).

- Learn about how to understand and choose coverage with Navigating CF

Share this article

Topics

Insurance

|

Managing Finances

15 min read

We want to hear from You

People with CF and their caregivers are invited to share how the cost of living with CF affects their daily lives and access to healthcare services. This research survey is limited to U.S. residents.